|

|

Checking in on Main Street valuations |

|

Over the past few months, as we released our reports on mid-market M&A (USA, UK), we’ve focused a lot of this newsletter on the insights drawn from mid-market valuation activity, looking at how buyers, sellers, and advisors are responding to changing economic conditions. (And a big thank you to everyone who has engaged with us on these topics, it’s been fascinating to hear your views.) But don’t worry, we haven’t forgotten about those owner-operated businesses who continue to be highly valued clients, partners, and friends of ours. So, this month, we’re returning to Main Street to analyse our latest data on this section of the market. This is a world we’re very passionate about and one that we continue to serve in a myriad of different ways. What follows is not a single thesis, but a rapid-fire snapshot of what we’re currently seeing across Main Street valuations on the bizval platform. These are observations rather than predictions, and you should think of them as a pulse check on how value is being expressed, discounted, and rewarded in this part of the market. Let’s dive in. |

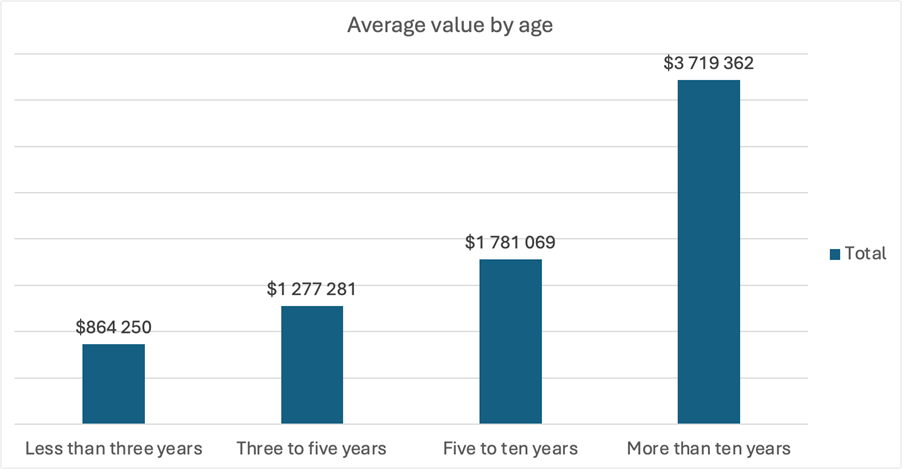

Business age: longevity still carries a premium

|

|

Average valuations increase materially with the age of the business. Companies less than three years old attract the lowest average values, while businesses operating for more than ten years are valued at more than double those under five years. But this is not simply about size. Longevity acts as a proxy for several risk-reducing factors that valuers consistently price in: survival through multiple cycles, established customer relationships, and proven cash-flow patterns. Takeaway: On Main Street, time in the market remains one of the strongest signals of resilience. Younger businesses continue to face a significant valuation discount, reflecting uncertainty rather than ambition.

|

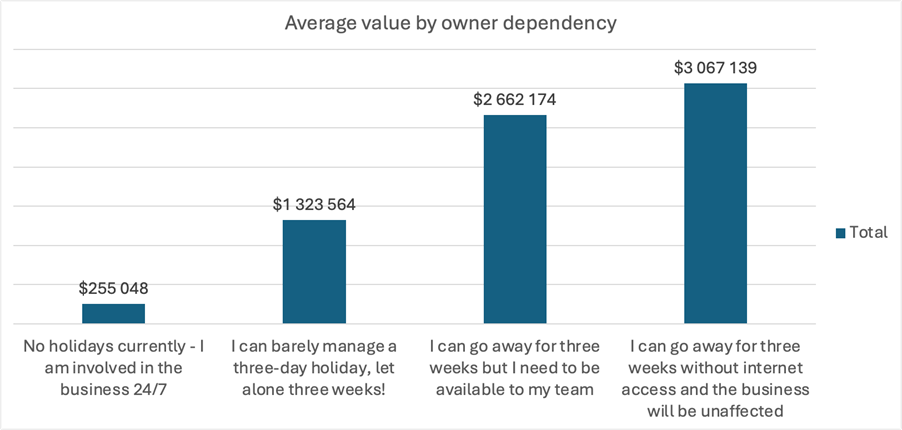

Owner dependency: a clear marker of perceived risk

|

|

One of the starkest valuation differentials appears around owner involvement. Businesses where the owner is involved full-time, with limited ability to step away, show dramatically lower average values than those that can operate independently. We’ve spoken about this a lot over the years, but it still remains an incredibly important concept for owner-operators. It’s critical that owners focus on systems, delegation, management depth, and operational repeatability as early as they can because, from a valuation perspective, owner dependency remains one of the clearest indicators of key-person risk and the market continues to price that risk decisively. Takeaway: Whether cause or consequence, owner dependency is consistently reflected in Main Street valuations. Businesses that rely heavily on a single individual remain more vulnerable to discounting. |

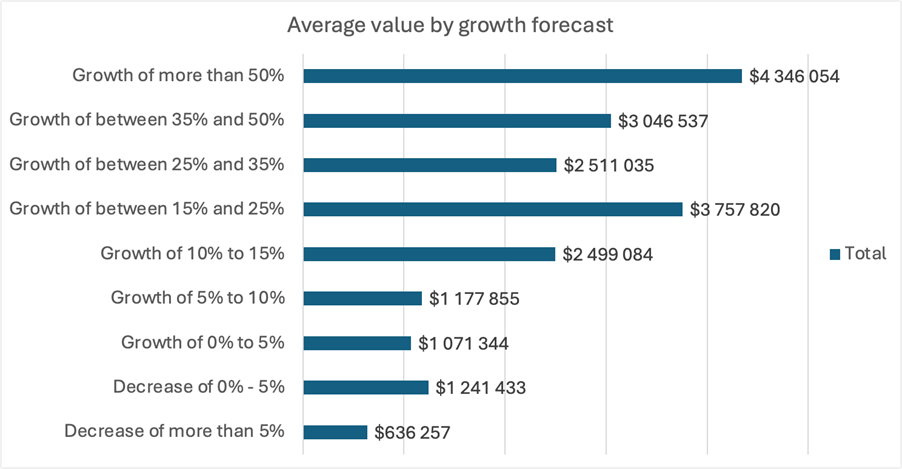

Growth expectations: credibility beats optimism

|

|

Valuations rise meaningfully where future growth is expected, but the relationship is not linear and can be a bit messy. More growth does not always result in a higher valuation. This suggests that credibility matters as much as ambition. Buyers and valuers appear more comfortable pricing growth that is plausible and supported by historical performance than aggressive projections that introduce execution risk. Takeaway: On Main Street, growth expectations still matter, but believable growth is valued more consistently than optimistic projections, and contraction is punished early.

|

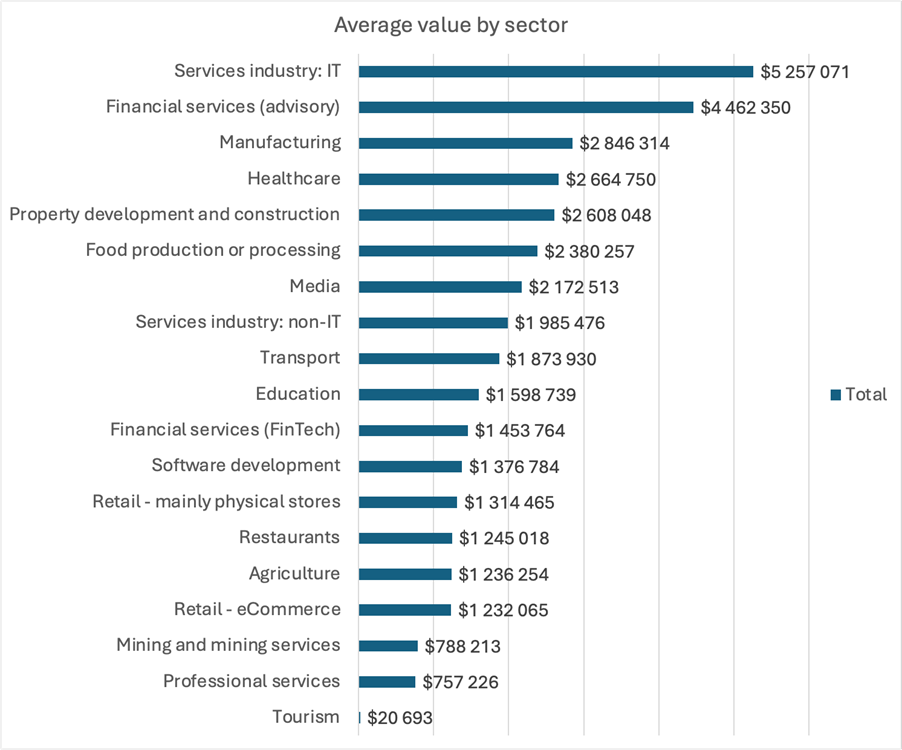

Sector snapshot: defensibility remains favoured

|

|

Average valuations vary widely by sector. Service-based and advisory businesses (particularly those with repeatable revenue and low capital intensity) continue to command higher average values than asset-heavy or margin-constrained sectors. This largely reinforces long-standing valuation dynamics rather than revealing new trends. Defensibility, recurring revenue, and pricing power remain highly valued characteristics, regardless of business size. What is going to be very interesting to watch over the next 12 months is how advancing AI and automation disrupts this value hierarchy. As agentic AI starts to become more capable and widespread, we might expect to see quite a different picture in a year from now. Only time will tell… Takeaway: Sector still matters on Main Street, but not in new ways. Familiar preferences for repeatability and defensibility continue to dominate valuation outcomes.

|

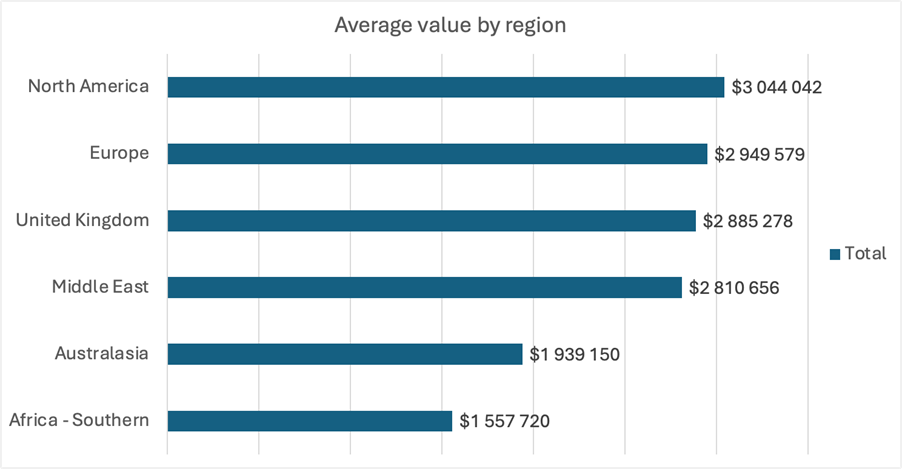

Geography: market depth still shows up in value

|

|

It’s no secret that average valuations differ meaningfully by region. Businesses in North America and Europe sit at higher average values than those in Australasia and Southern Africa. But these differences should never be read as a reflection of business quality alone. Market depth, buyer pools, access to capital, and transaction liquidity all influence how value is expressed in different regions. For Main Street businesses, geography continues to shape both opportunity and constraint, particularly when it comes to exit optionality. Takeaway: Regional valuation gaps persist, reflecting structural market factors rather than purely operational performance.

|

What this snapshot suggests

|

Taken together, these observations point to something notable: the drivers of value have stayed mostly the same. Across Main Street, the market continues to reward:

Longevity and survival Reduced key-person risk Credible growth Operational independence Transferability At the same time, the penalties for fragility, concentration, and uncertainty remain significant. Of course, Main Street data is inherently noisier and more volatile than mid-market data, and we’re only pulling from our internal data for this analysis, but there is a lot to be gleaned from these snapshots. As we continue to monitor valuation activity across Main Street and the mid-market, these smaller-business signals provide useful context for understanding how risk and value may evolve further up the market. We’ll continue checking in and bringing you insights as we unearth them. But if you have any thoughts, comments, stories, or ideas of our own - we’d love to hear them! Just reply to this email and let us know what you think.

|

|

|

Recent podcasts

|

|

|

|

Why private markets are getting a liquidity makeover.

In this episode, Graham speaks with Mason Doick, Head of Corporate at JP Jenkins, about what's quietly changing in the world of private company ownership, and why founders, investors, and advisers should be paying attention. The conversation gets into the mechanics of how secondary markets for private shares actually work, who they're suited for, and the trade-offs founders often overlook when thinking about stakeholder structures and dilution. Listen Here.

|

The value of peer boards in leadership decision-making.

In this episode, Graham speaks with Eduan Steynberg, owner of The Alternative Board in the Western Cape. The conversation walks through Eduan’s career journey, before focusing on the value of peer boards for getting real, hard-fought advice, emotional support, accountability, and practical frameworks that can help business owners achieve their version of success. They also discuss some of the most common challenges that owners face and how to overcome them. Listen Here.

|

|

|

Check out our new website

|

|

After a lot of late nights and even more rounds of feedback, we're excited to announce that we’ve officially launched our new website! It's more than a fresh coat of paint because it reflects how bizval has grown, where we're headed, and the kind of clarity we think business owners deserve from the moment they land on our page. Take a look around at bizvalglobal.com and let us know what you think!

|

|

|

bizval featured in They Got Acquired's 2026 M&A outlook

|

We were glad to be included in They Got Acquired's roundup of M&A trends to watch in 2026, and the themes running through the piece are very much consistent with what we're seeing on the ground. Sophisticated buyers, a sharper focus on fundamentals, and the growing importance of preparation aren't just predictions; they're already shaping how deals are getting done. A big thank you to the They Got Acquired team for including us alongside some great voices in the industry. If you missed the Q1 2026 US M&A report they mentioned, check it out here. But otherwise be sure to read the They Got Acquired post - lots of good stuff inside! |

|

|

Winning the Away Game: Why bizval exists

|

We enjoyed this Winning the Away Game story on Graham Stephen and the early experiences that shaped bizval’s mission. It’s a sharp reminder that value is built long before an exit, through transferability, resilience, and removing single points of failure.

A valuation is less a once-off event, and more a regular check-in on whether your business can stand on its own.

Read the full story here. |

|

|

Attending the 2026 Ansarada Dealmakers Awards

|

|

One of the bizval team, Boitumelo Boikhutso, recently attended the 2026 Ansarada Dealmakers Awards and penned an insightful blog post on the experience. Here’s a brief summary: “I observed a South African M&A market that remains active and disciplined, with transactions increasingly structured, data-led, and supported by technology-enabling diligence. As deal complexity rises, independent valuation insight continues to play a central role in anchoring negotiations, informing strategy, and supporting long-term value creation.” Read the full post here.

|

|

|

|

|

|